Author’s Note: A great introduction to MMT can be found at https://findingmoneyfilm.com/. I suggest it as a prerequisite to the essay that follows.

Part I. Flow and Disruption

Author’s Note: This is not original research, but the result of an extended conversation with ChatGPT, in large part fueled by my interest in Modern Money Theory (MMT) and a desire to understand how a reserve currency operates at the simplest level. If you are interested in a deeper dive, I suggest reading “The Deficit Myth,” by Stephanie Kelton.

When an American buys a television, a phone, or a pair of shoes made overseas, it feels like a simple transaction. Money leaves your account, and a product shows up at your door. But behind that everyday purchase lies one of the most powerful — and most misunderstood — engines of the modern world. That engine is the U.S. dollar.

For decades, the United States has enjoyed a unique position in the global economy. It can buy physical goods from the rest of the world in exchange for pieces of paper — or more precisely, digital bank entries — that it alone has the authority to create. Other countries not only accept these dollars; they actively compete to earn them.

On the one hand, this system has brought enormous benefits to Americans, including low prices, global influence, and access to a nearly endless stream of imported goods. On the other hand, it has also produced deep regional inequality within the United States, weakened the social fabric, and fueled a political backlash reshaping American democracy.

To understand why this system persists, why it’s now under strain, and what it will take to repair it, we need to follow the dollar from the moment it leaves your wallet to the moment it circles back as a U.S. Treasury bond — and then trace the social and political consequences that follow, highlighting the dollar’s central role in global trade and domestic stability. What actually happens to the money is far from obvious.

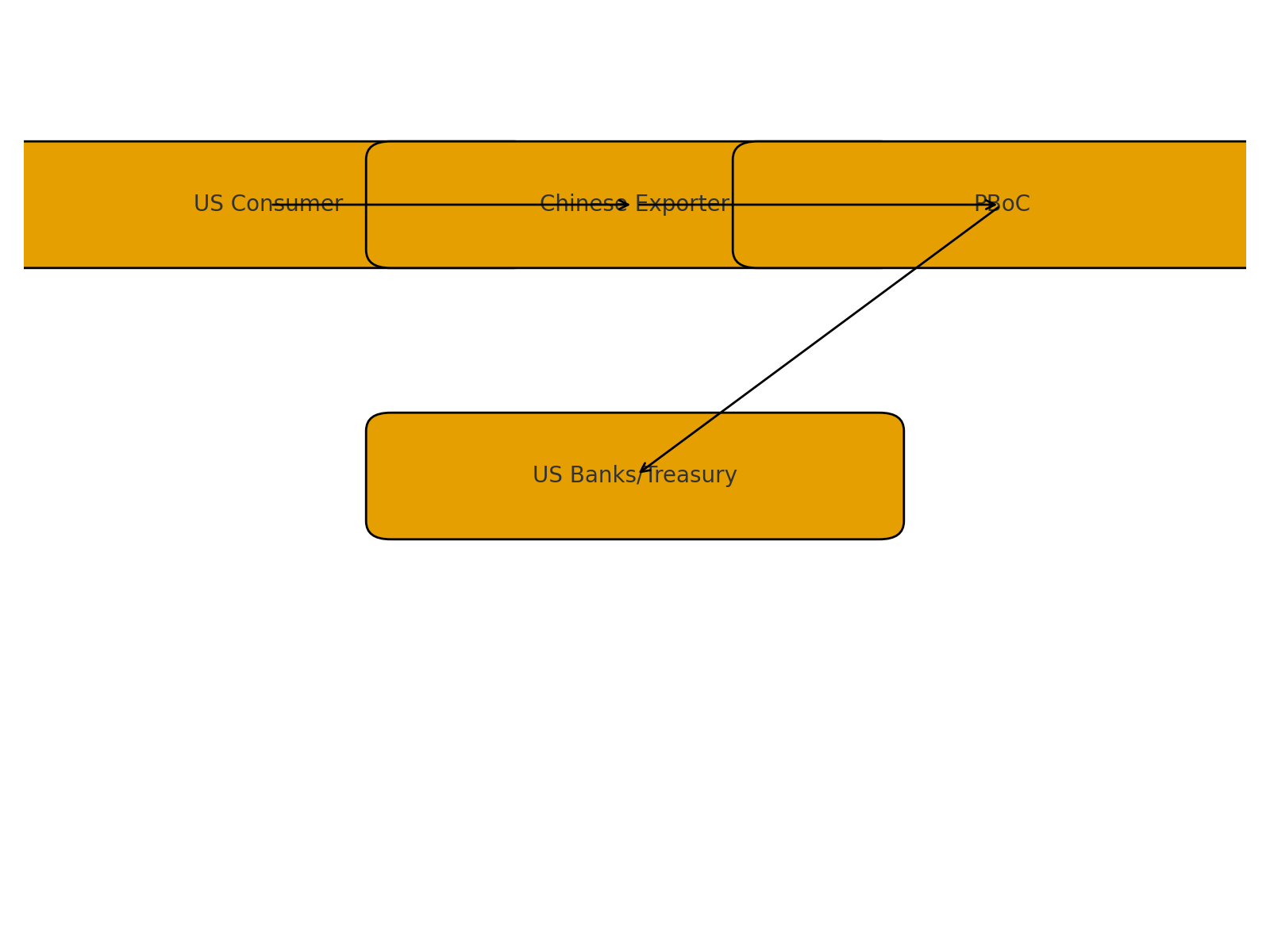

Imagine an American buys a $100 product manufactured in China. The $100 is transferred first to the Chinese exporter’s bank account. But those dollars are not usable inside China. A factory in Guangdong can’t pay its workers in U.S. currency. So the exporter exchanges dollars at the People’s Bank of China, China’s central bank, for the local currency, the yuan.

The exporter now has yuan to operate on the home front. And China’s central bank now holds $100. But even China can’t spend those dollars domestically. They are foreign currency. They’re only good abroad. So what does China do?

It invests them back into the United States. Most often, China uses those dollars to buy U.S. Treasury bonds — effectively lending the money back to the U.S. government. And with this transaction, the dollar has completed its round trip: from an American consumer to a Chinese business to China’s central bank, and finally back to the U.S. financial system.

At this point, you can see that something unusual is happening. The United States buys physical goods — televisions, cars, electronics — and the dollars it spends end up right back in the country, parked safely in government debt. China, in turn, ends up holding U.S. assets, not goods.

It is worth repeating. The U.S. receives products. China receives dollars. The dollars return home. You can picture this visually as a loop — a flow of money out of the U.S. and back again, powering global trade.

At first glance, this seems like the world’s most favorable deal. And in many ways, it is. But China doesn’t do this out of generosity. It does it because the system serves its interests just as powerfully as it serves America’s.

If China can’t spend dollars internally, why does it still accumulate them by the trillions? Because the arrangement delivers crucial benefits.

First, it delivers jobs. Export industries employ tens of millions of Chinese workers. Social stability depends on employment; employment depends on exports; and exports depend on a competitive currency. China buys dollars and holds Treasuries in part to prevent the yuan from rising and making its products more expensive abroad.

Second, it delivers industrial growth. Exporting manufactured goods has been the backbone of China’s modernization. Earning dollars gives China the ability to buy foreign machinery, semiconductors, food, and, most importantly, oil — none of which can be purchased with yuan.

Third, it delivers financial protection. Large reserves of dollars and Treasuries help China defend its currency during global shocks. They are a buffer against crisis.

So while it may seem odd that China ships products to the U.S. in return for claims on American debt, those claims are central to China’s economic strategy. The system is not charity; it’s a calculated partnership.

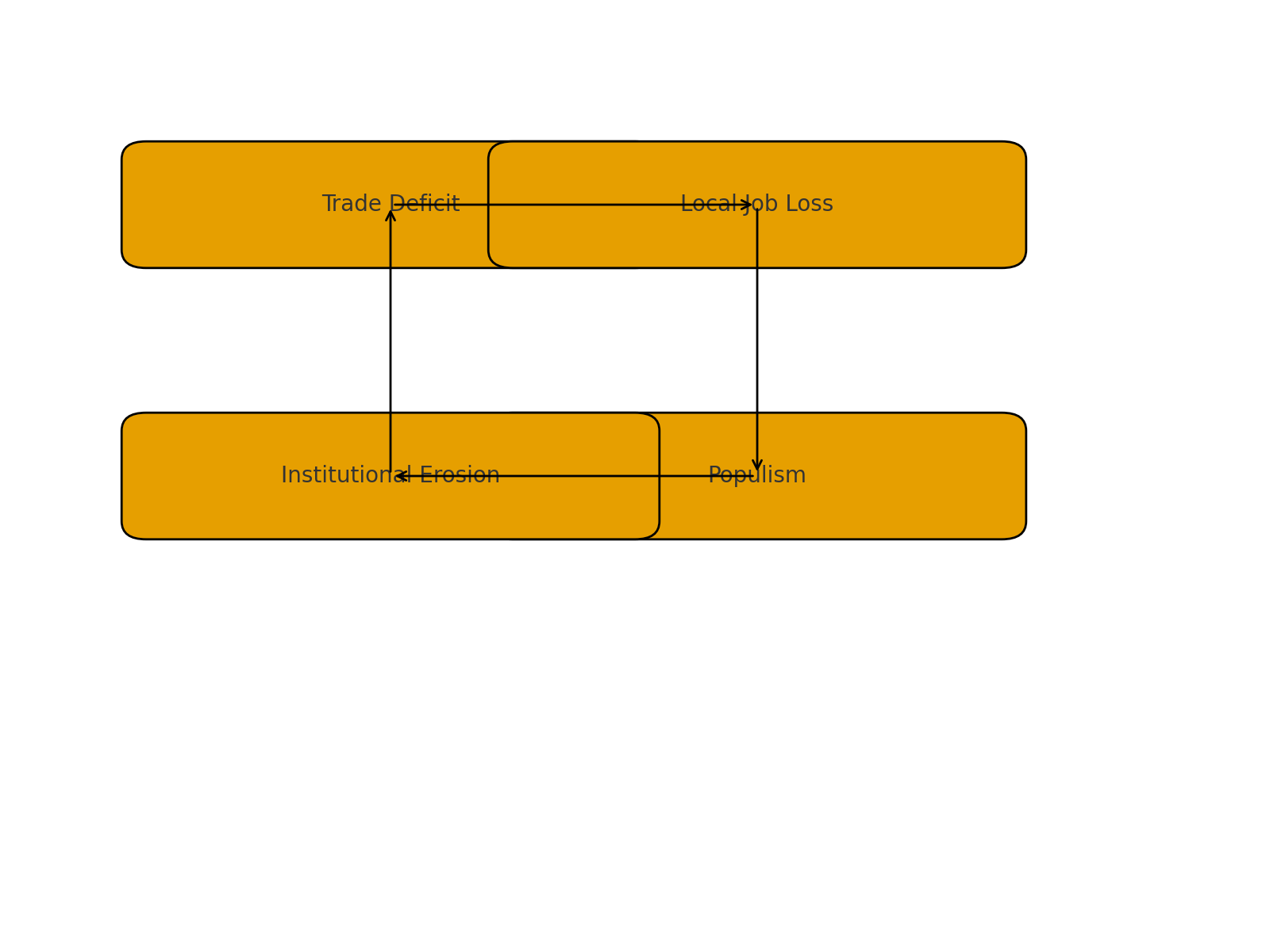

For the United States as a whole, buying foreign goods cheaply is a clear win, but not everyone wins equally. Over time, the steady flow of inexpensive imports, made possible by the dollar’s global dominance, contributed to the erosion of American manufacturing. Factories closed, and jobs disappeared. Some regions reinvented themselves, but some never recovered.

This weakens the U.S. from within. This regional decline created something more profound than economic loss. It produced:

- wounded pride

- declining local services

- fraying communities

- intergenerational pessimism

- anger at both elites and institutions

The anger is not abstract. It is political fuel. Places where jobs disappear become places where trust in government collapses. That collapse feeds populism, which in turn destabilizes American institutions, from foreign alliances to democratic norms, and makes the U.S. a less predictable global actor. This, in turn, undermines international confidence in the very system that supports American power.

This is the danger: A system that economically strengthens America as a nation is politically weakening it from the inside. Escaping this negative cycle doesn’t require dismantling global trade or abandoning the dollar’s central role. Instead, it demands policies that redirect the benefits of America’s financial power into rebuilding communities and addressing systemic issues.

Since the United States has unmatched financial capacity, it should use that capacity to rebuild the social foundation that keeps the whole system stable. This means focusing not on protectionism but on resilience:

- investing in workers whose industries are disrupted

- supporting communities left behind by global shifts

- building strategic industrial capacity at home

- modernizing infrastructure

- reducing political incentives for polarization

- stabilizing the country’s role on the global stage

It also means reframing the purpose of America’s financial power. Issuing the world’s currency is a privilege. It should not be used solely to inflate asset prices or finance private consumption. It should be used to reinvest in the public goods, education, health, infrastructure, and innovation that make American society strong.

The United States, more than any nation in history, can finance its own renewal. It can borrow in its own currency. It can attract global savings on demand. It can run trade deficits without destabilizing its exchange rate. These are extraordinary advantages.

But the preservation of this system depends on the social cohesion that underpins it. Without a stable domestic base, global leadership becomes harder to sustain. Alliances become shakier. Markets grow more nervous. The political pendulum swings more violently.

If America continues on its current path, in which the economic benefits of global trade are not broadly shared, then the dollar system will erode, slowly but inevitably. Not because China destroys it, but because Americans lose faith in the structure of their own society.

The choice is simple. Use the extraordinary privilege of the dollar equitably, or watch that privilege slip away. There is no need to surrender the benefits of the dollar as a reserve currency as long as the bellows of inequality are dismissed. The global system runs on trust, and trust begins with a society that believes in itself.

Part II. The China Syndrome

Author‘s Note: The rest of this article was added as an addendum in response to the observation “They (most people) feel like we have to get rid of that debt or China is gonna come take us over because we owe them so much.”

Every few years, headlines warn that China “owns our debt,” implying that the United States is financially beholden to its biggest creditor. The image is dramatic: America, one market tantrum or a militarily motivated financial attack away from collapse. From the standpoint of MMT, that story misunderstands how a sovereign currency works. The U.S. doesn’t borrow from China. China saves in U.S. dollars. And that distinction changes the entire picture.

When China buys a U.S. Treasury bond, it is not extending credit, as a bank does when it lends money to a borrower. It is simply exchanging one form of dollar asset (reserves) for another (a Treasury bond) to earn a bit of interest. In simpler terms, it is changing a checking account into a savings account. Operationally, China’s dollar holdings never leave the Federal Reserve system. They are entries in a spreadsheet representing the dollars China has already earned from exporting goods to Americans. So instead of “China lends, America borrows,” the more accurate phrasing is: “China saves in the currency that America alone can issue.” That’s not dependence. Its interdependence is built on the United States’ unique monetary position.

Foreign Treasury holdings are the mirror image of America’s trade deficits. Every time the U.S. runs a trade deficit by importing more than it exports, another country ends up holding the dollars it receives. Those dollars must go somewhere. They don’t pile up in warehouses or disappear. They are recycled into U.S. financial assets. From an accounting point of view, the U.S. “national debt” is simply the record of all those accumulated savings. It’s the flip side of the world’s desire to hold safe, liquid assets. Seen through that lens, the question isn’t “What happens if China calls in its debt?” The question is “What are we doing with the real resources and productive capacity that this global savings makes possible?”

The United States owes nothing that it can run out of. It owes dollars, which it alone can create. What it cannot print are the things that dollars are meant to mobilize:

- engineers and teachers,

- bridges and energy grids,

- functioning institutions,

- and a cohesive public willing to work toward shared goals.

From an MMT perspective, those are the proper limits of American power. A nation that can issue its own currency can never be forced into insolvency. But it can run out of trust, competence, and productive energy. And those deficits — not the financial ones — are the real danger.

Privilege leads to complacency. The dollar’s role as the world’s reserve currency has insulated Americans from many of the pressures faced by other nations. The U.S. can import goods cheaply, borrow without fear of default, and sustain persistent deficits that would bankrupt smaller economies. But that very privilege can dull the impulse to invest in domestic productivity. Why rebuild factories or trains when the world is eager to send you goods in exchange for paper assets? Why strengthen social insurance when foreign savings keep interest rates low? Over time, this convenience becomes a trap. The U.S. has grown accustomed to buying everything except social stability.

If MMT is correct, we are worried about the wrong thing. America’s problem isn’t “debt.” It’s the underuse of its own productive potential — both physical and human. A country that issues the world’s reserve currency has enormous fiscal space. But that space is wasted if it’s used to inflate asset prices rather than build capacity — if it finances share buybacks instead of semiconductor fabs, speculation instead of education, or political polarization instead of social trust. The fundamental constraint on American prosperity isn’t the Treasury’s balance sheet. It’s the nation’s ability to mobilize resources for a shared purpose.

Let’s reframe the national balance sheet. Imagine the national balance sheet as having two sides: financial liabilities on one side and tangible assets on the other. On the financial liability side, the U.S. owes the amount of the treasury bonds held by the world; on the tangible asset side, the American people, infrastructure, industry, and institutions. We worry endlessly about the left side — the dollars and bonds. But the value of those liabilities is guaranteed by the strength of the right side. When the right side erodes — when education falters, bridges crumble, and trust decays — the left side becomes riskier, not because the U.S. can’t pay, but because its society can’t hold together. That’s the paradox of the dollar system: the stronger America’s financial dominance grows, the more it must consciously reinvest in the social and productive base that makes that dominance legitimate.

MMT doesn’t deny limits; it relocates them. The accurate measure of solvency for a sovereign currency issuer is not its ability to pay, but its ability to produce, govern, and cohere. If foreign savings represent the world’s confidence in the dollar, then every broken bridge, underfunded school, and disillusioned voter is a silent drawdown on that confidence.

In the end, the global savings glut sitting in Treasuries is not a sign of American weakness. It’s a sign of trust — trust that the U.S. will remain a functioning, stable, productive society worthy of holding claims against. The risk is not that China will cash in those bonds. The risk is that America will stop deserving that trust.

Part III. The 10-Point Plan

Author‘s Note: I lied. There is an addendum to the addendum—time to move beyond China. I wanted to factor in the environment, AI taking over the job market, and the continued imbalance between developing and developed countries into the MMT conversation. After all, not much of a plan if it doesn‘t address the significant social and environmental issues confronting the world. A friend once asked me what I would do if I were king of the world. The 10-point plan is my answer (until the next addendum, anyway).

If the valid constraint on a sovereign nation is not money but real resources, then we must define those resources broadly. They are not only labor, machines, and raw materials — they include clean air, stable climates, fertile soil, biodiversity, and the human trust that allows societies to function. In this light, America’s reserve-currency privilege is not just an economic tool. It is a planetary responsibility. The dollar system, after all, organizes the world’s production, consumption, and debt. Its architecture shapes how we treat both people and the planet.

Three global challenges make this clear: environmental externalization, technology and the future of work, and ending the extractive relationship with developing nations.

Free trade agreements and global supply chains have allowed wealthy countries to consume goods without accounting for the pollution embedded in their production. Factories that once polluted the Midwest now pollute Southeast Asia. The carbon, however, doesn’t respect borders. This is a hidden cost of the dollar system: the U.S. runs trade deficits in goods, but trade surpluses in pollution. The externalization of environmental damage props up the illusion of low prices at home while degrading the global commons that underpins all economic life. If MMT tells us that real resources, not money, are the limit, then climate stability is the ultimate fundamental constraint. The atmosphere cannot be bailed out with dollars. No fiscal space is infinite if the planet’s carrying capacity collapses. A reformed global monetary system would therefore measure deficits not just in dollars, but in ecological terms. America’s “full employment” must mean employing people to heal, not merely to produce — restoring soils, building green infrastructure, rewilding damaged land, and decarbonizing energy.

For a century, productivity gains have come from augmenting human labor with machines. But AI marks a turning point: it can replace labor entirely in many sectors. The traditional MMT prescription of a job guarantee, government employment at a living wage to ensure full labor utilization, might stabilize society in the near term. Automation will ultimately make “jobs for all” economically redundant. When machines can perform nearly all marketable tasks, the purpose of income shifts from rewarding work to ensuring participation in society. At that point, a Universal Basic Income (UBI) becomes not just welfare but economic infrastructure — the digital bloodstream that keeps demand, creativity, and dignity circulating. UBI, funded through sovereign currency issuance, is entirely consistent with MMT principles. It provides a baseline floor of aggregate demand, preventing collapse when private employment shrinks, and allows people to pursue education, caregiving, art, and community projects outside the wage system. The challenge is not affordability — the U.S. can issue the dollars. The challenge is designing a moral economy where productivity gains from AI are shared rather than hoarded.

The international monetary order still rests on colonial logic. Developing countries borrow in foreign currencies they do not control, often dollars, and are forced into austerity when export revenues fall. The result is a global pattern in which the periphery exports cheap labor and raw materials, while the core exports debt and financial instability.

MMT offers a different lens. Every country that issues its own currency has fiscal space limited only by its real resources and productive capacity. The problem is that most developing nations lack monetary sovereignty: their currencies are not trusted globally, so deficit spending risks capital flight and currency collapse. If the U.S. wants a stable, equitable world order — one less vulnerable to debt crises and migration pressures — it could extend proxy monetary sovereignty to partners. That means providing direct access to dollar liquidity for investment, not as loans tied to austerity, but as cooperative credit for development, climate adaptation, and infrastructure. Call it a Global Green Credit System: nations could run moderate, MMT-style deficits in a stable reserve currency while building real capacity at home. Instead of the IMF enforcing fiscal contraction, an international public bank could finance growth in ways that are ecologically sustainable and locally governed. This would replace the extractive global balance — dollars for sweat and minerals — with a regenerative one: dollars for development, resilience, and shared prosperity.

Here is a ten-point plan to meet the full scope of our economic, ecological, and moral responsibilities.

1. Insure People, Not Sectors

Build a resilient social foundation: universal healthcare, robust unemployment insurance, childcare, and transition income for displaced workers. Security enables adaptation.

2. Create a Dynamic Job Guarantee

Guarantee public work at a living wage in fields that rebuild the nation’s real wealth — renewable energy, conservation, caregiving, and civic infrastructure. Employment becomes a tool for regeneration, not make-work.

3. Develop a Path to Universal Basic Income

As automation advances, phase in a permanent income floor. UBI ensures that technological abundance translates into human freedom rather than precarity. Productivity gains become public dividends.

4. Invest in Real Productive Capacity

Direct federal spending and public investment toward strategic industries: semiconductors, energy storage, AI governance, biomanufacturing, sustainable agriculture, and logistics. Deficits that build capacity are not costs; they are investments in resilience.

5. Anchor Growth in Environmental Accounting

Integrate carbon, biodiversity, and pollution metrics into fiscal and trade policy. Use the dollar’s power to set global green standards — rewarding nations and firms that internalize ecological costs. Monetary sovereignty means environmental responsibility.

6. Rebuild Infrastructure for a Sustainable Century

A Green New Deal scale transformation: high-speed rail, a smart grid, water systems, reforestation, urban cooling, and flood defenses. Public investment is both a climate mitigation and an employment engine.

7. Democratize Technological Progress

Treat data, AI models, and essential digital infrastructure as public goods. Establish public options for AI services and open innovation platforms to ensure that technology amplifies human welfare rather than concentrates wealth.

8. Reform Global Finance for Shared Sovereignty

Work with allies to create regional clearing unions or dollar proxy systems that allow developing nations to run safe deficits in pursuit of full employment and a green transition. Replace debt traps with development credit lines tied to real outcomes, not austerity targets.

9. Rebuild Political Cohesion at Home

Adopt electoral and campaign reforms that reduce polarization and capture. Social spending must be matched by democratic renewal — people must see that government works for them, not just for markets.

10. Use the Dollar for Regeneration, Not Extraction

Reimagine the “exorbitant privilege” as a global stewardship role: If the world saves in dollars, those dollars should fund planetary healing, human flourishing, and shared security. Fiscal capacity is moral capacity.

In the end, MMT’s insight is not that money is infinite, but that our imagination of what’s possible has been artificially constrained. A nation that issues the world’s reserve currency can marshal resources on a scale unmatched in human history. The question is no longer “Can we afford it?” but “What do we choose to build?” If we use that power to restore ecosystems, share technological prosperity, and rebuild social trust — then the dollar’s global role becomes not just an instrument of hegemony, but a tool of regeneration. If we fail and continue treating money as scarce while the planet and people are expendable, then no financial architecture will save us.